Sierra Leone, which earns 85% of its foreign exchange from mineral exports, has been devastated; economies as big as South Africa’s and Nigeria’s are also struggling. Now, leaders and activists are trying more nationalist tactics against the resource curse.

Commodity price crash. Endemic corruption. Rebellion. Mutiny. Coup d’état. Invasion. Anarchy and atrocities. West African, British and UN intervention forces. Peace talks. Special court tries rebel leaders. New mining investors. World’s fastest-growing economy in 2013. Ebola outbreak. Mining companies stop production, and two companies collapse. World’s fastest-shrinking economy in 2015. Commodity price crash. How many other countries have been hit by such an unrelenting cycle of attacks and setbacks over the past three decades?

Five years ago, a boom was on the horizon. West Africa was the new frontier for iron ore, and Sierra Leone was at its epicentre. Reckoned to have over 10% of the world’s reserves of high-quality iron ore, West Africa would soon be exporting more than 500m tonnes per year. Miners went through a platinum boom, but never set up an emergency fund for the bad times.

Instead, the economies of Sierra Leone and its neighbours, Guinea and Liberia, are on hold after the world price of metals crashed in the past year. These economies, and many others across Africa, are locked in the commodity trap with few alternative sources of income. Two of the biggest mining companies in Sierra Leone went out of business last year and a third is at a standstill as thousands of workers were laid off.

So what went wrong?

From his fourth-floor office a stone’s throw from the giant Cotton Tree, which dates back to the founding of Freetown in 1792, Herbert M’cleod, one of Sierra Leone’s leading economists, sets out his prognosis: “It is bad policies and bad management that have brought us here […]. The way out is to link the mining business with the wider society, with jobs, training, electricity, roads. The mining sector cannot be left on autopilot […]. It has to be integrated into the rest of our development plans.”

Beyond the $1.5bn that iron ore was set to generate from royalties and other taxes each year, there should have been a huge boost to the local economy as companies set up to service the industry. “That didn’t happen in the way we wanted it,” M’cleod explains. Part of the problem was the type of companies that came in. “As a post-conflict country with weak institutions, our mining industry attracts high-risk investors and bottom-feeders.”

Bought promises

The government was faced with a cruel choice, says M’cleod: “Wait for the world-class companies who take their time to come in […] or buy the promises of immediate mine development, revenues and jobs that the smaller and less-known players offer.”

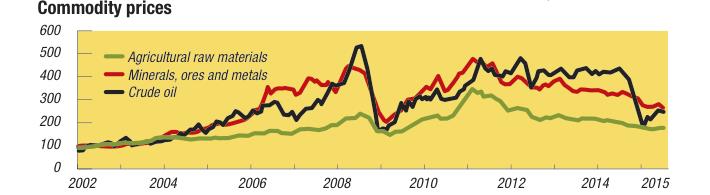

President Ernest Bai Koroma’s government chose the latter. Companies such as Frank Timis’s African Minerals and another British-listed outfit, London Mining, arrived in Sierra Leone a decade ago, winning mineral rights across vast areas and generous tax concessions while facing little operational scrutiny. Of the two companies, Timis’s proved the savvier operator and the faster to take advantage of strong prices for iron ore, which reached a high of $190/tn in 2011. Iron was trading for about $57/tn in March 2016. Timis persuaded China’s Shandong Iron & Steel Group to take a 25% stake in the project and invest some $1.5bn to develop the mine in early 2014.

Eventually, a combination of the Ebola outbreak – which froze much of the country’s economy – chronic mismanagement and the 2015/2016 commodity price crash pushed both African Minerals and London Mining out of business. The closures cost more than 15,000 jobs for those directly working for the mines and tens of thousands more for people providing equipment and services.

Timis’s mine started producing lowgrade ore – known in the trade as ‘mud’ – at Tonkolili in November 2011. As operations began, the value of the company’s share price skyrocketed on the London Stock Exchange’s Alternative Investment Market to $3.5bn.

As others were caught up in the breathless pace of the commodity supercycle, activists and trade unionists asked awkward questions about how Sierra Leone’s iron ore industry was being run. For the government, the numbers from the International Monetary Fund (IMF) and World Bank told a good story: gross domestic product grew from 6% in 2011 to 15.2% in 2012 and then to 20.1% in 2013, making Sierra Leone the world’s fastest-growing economy.

Abu Brima, executive director of the Network Movement for Justice and Development, urges Sierra Leoneans to look beyond the headline figures: “How much is our country really earning in terms of jobs and investment? These are valuable resources that were parcelled out to companies with little or no track record […]. There was no bidding process and minimal accountability. The companies who got the licences also got huge tax concessions, which hit the revenues due to the government.”

Not only was the country losing much-needed revenue, Brima adds, but the mines were not being managed in a way that would create jobs and develop the economy: “Expensive sub-contractors were brought in from outside for tasks that locals could do.”

At the same time, problems were mounting at the mines. Elsewhere in the African Minerals’ concession area, police were accused of carrying out a bloody crackdown in Bumbuna in April 2012 against striking workers. At the centre of it was Moses Gbondo, general secretary of the Mining and Allied Services Employees Union. He tells The Africa Report that he and his colleagues had established an alternative to the long-standing United Mineworkers’ Union, which had not organised credible leadership elections in decades. “The workers at the African Minerals mine [in Bumbuna] were striking about conditions and protesting that they had not been allowed to join the trade union of their choice,” he explains.

Strikers gunned down

The situation spun out of control, according to Gbondo, as it had in the deadly Marikana clashes at Lonmin’s platinum mines in South Africa in 2012. “The security guards and police started shooting, killing one worker and wounding several more.”

For Esther Finda Kandeh, who runs a campaign group, Women on Mining and Extractives, the shootings at Bumbuna are part of a wider pattern of repression in the country’s mines. “We’re trying to improve conditions for women in mining, their chances of jobs in the sector […]. Currently, they just get low-level roles in services or cooking. We want to get them better-paid administrative jobs as well.”

Finda Kandeh’s organisation also represents women living with their families in mining areas who complain they are arbitrarily forced to move at short notice: “In the Tongo field last year, in the diamond areas, the companies forced many people from their homes so they could start blasting […]. People had to relocate to areas where the farming was not as good. The walls of their houses were cracked, and afterwards there were water shortages but no compensation.”

Making a case for change to the government or the mining companies is an uphill struggle, according to Brima and Finda Kandeh. With commodity prices and export revenues crashing, they say the government has little interest in taking on the mining companies. On some issues, there seems to be collusion between state officials and the companies.

New policy

It is more about realism, insists deputy mines minister Abdul Ignosi Koroma when asked why the mining contracts were so generous to the companies: “We have to look at the marketplace. When no one wants to explore because the prices are low […] of course the contracts will not be good.” The government’s dealings with African Minerals were based on practical necessity, he argues. “They did the aeromagnetic surveys [and] produced data eventually showing reserves of 12.8bn tonnes of magnetite ore. No one else would take that on.”

Koroma is confident the mining sector will bounce back over the next five years: “We are due to announce our new core minerals policy next month [April], which should reassure investors and increase revenues for government.”

Officials drawing up the new policy consulted widely with companies, community and workers representatives, said Koroma, adding that the sector would be more efficiently managed. Last year the government established the National Minerals Authority as a professional agency to implement and monitor policy but also to improve the accountability of the sector. Although the government is not comprehensively renegotiating contracts in the wake of the price crash, it will scrutinise new contracts far more avidly, bringing in legal advisers from the African Development Bank and other agencies.

Iron ore production is due to restart at the Tonkolili mine, which is now 100% owned by Shandong. Its legal adviser told us the company has been discussing grants to community organisations and severance payments to workers. Only Sierra Rutile’s mineral sands operation, run by John Sisay, a cousin of President Koroma, has been making money and increasing production. But that is not enough to steer the economy out of the doldrums. It is forecast to grow just under 1% this year, according to the IMF. Inflation is set to rise at five times that rate, partly due to the weakening exchange rate of the leone against the United States dollar.

The arguments over resource nationalism, land use and beneficiation, which are getting more insistent in Sierra Leone, have been central to politics in South Africa for the past decade. This is partly because of competition for working-class support between the African National Congress (ANC) party in government and the radical Economic Freedom Fighters (EFF) under Julius Malema, who wants nationalisation of the mines without compensation. Sometimes, corporate South Africa struggles to differentiate between Malema’s radicals and the ANC’s resource nationalists.

That was clear at this year’s Mining Indaba, which drew between 6,000 and 7,000 participants to Cape Town in February to meet the industry’s major corporate and political figures. Once one of the world’s top mining countries, South Africa is fast slipping down the rankings, said officials at the Indaba. Some 47,000 mining jobs were cut in the sector between 2012 and 2015.

The once-mighty Anglo American Corporation, which now includes the former diamond cartel De Beers, plans to lay off 85,000 of its workers worldwide over the next five years, which will shrink its workforce to 50,000.

Carnage

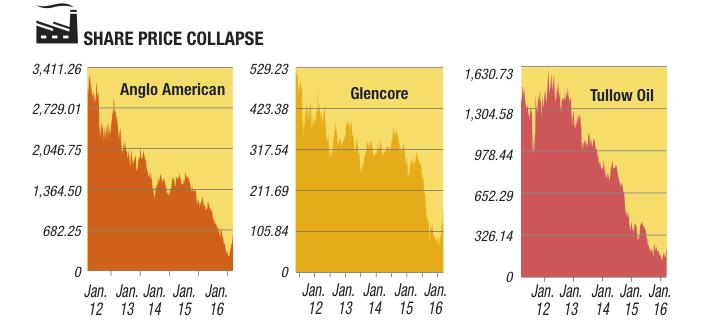

Mark Cutifani, chief executive of Anglo American, told the Indaba about the carnage in the mining industry wrought by the price crash. At the beginning of 2013, the market capitalisation of mining companies listed on London’s FTSE 100 index was $555bn; by 1 January this year, it had fallen to $169bn. Global mining stocks had lost $1.4trn in value since 2011.

With export revenues crashing, the government has little interest in taking on the mining companies

To that pattern can be added the effects of the worst slowdown in emerging-market economies since 2009. Africa is being hit not just by lower commodity prices but by capital outflows. From 2009 to 2014, some $2.2trn flowed into developing economies, partly because of quantitative easing and historically low interest rates in rich countries. That drove capital into developing economies: market capitalisation of the Johannesburg Stock Exchange nearly tripled between 2009 and 2014; capital markets in Nigeria, Ghana and Kenya followed suit.

Capital flows are turning negative for the first time since 2006. In 2015 there were net outflows from developing economies totalling $600bn–about a quarter of that is coming out of Africa. The biggest outflows have been through the banks: international banks are set to cut their credit debt service and weaken currencies, deplete reserves and depress asset prices. This adds up to serious damage to the real economy in Africa.

All this is a dangerous cocktail for the ANC government, but also for companies based in South Africa. Johannesburg-based British mining company Lonmin is in chronic financial trouble, which it blames on falling demand for its platinum; its workers blame mismanagement. In August 2012, police shot dead 44 people at Lonmin’s Marikana mine after a bitter dispute for recognition by the Association of Mineworkers and Construction Union (AMCU).

Marikana still haunts

Soft-spoken Thumeka Magwangqana chairs Sikhala Sonke, which supports the widows whose husbands died in the massacre, and says the community is haunted by the shootings and the threat of more job losses: “The last time we heard about any retrenchments here in Marikana was in January. I have heard stories of a mine like Samancor closing, and they are retrenching hundreds of people. This is terrible. We just do not know what the future holds, and it’s very stressful for us and the workers. The widows of the Marikana massacre are now working at the Lonmin mine [they replaced their husbands] and they have said nothing to them now about any retrenchments.”

John Capel, executive director of the Bench Marks Foundation, which monitors corporate performance, faults companies for failing to provide for mineworkers during price slumps: “[The mining companies] went through a platinum boom in the last 20 years and made returns of over 30%, but they never set up an emergency fund for the bad times.” He adds: “It is always workers who face the brunt in a commodity downturn. At least 45,000 [platinum] jobs have been lost since 2007, now perhaps 50,000 or more.”

Companies should think harder about how they can use platinum in local manufacturing processes, Capel argues, to create more economic linkages. For now, he says, companies seem to recognise few responsibilities, either to the workers they are laying off or to the degraded environment they leave behind when they end their operations. Mining has been at the centre of South Africa’s history and is inextricably linked to politics. The latest policy proposals to spread the benefits of the country’s mineral riches are rattling all but the most robust and innovative investors.

Botswana, where close collaboration between government and Anglo American/De Beers has assisted the development of a diamond-cutting and polishing industry, is held up as an example of practical resource nationalism. Sierra Leone’s M’cleod, who worked in Gaborone for many years, said the local environment – with its excellent transport, communications and energy provision – had very specific advantages.

“Local content policy should strengthen local business to be more competitive when bidding for contracts,” M’cleod argues, “rather than specifying percentages of local content in mining operations.” The key, he adds, was sustainability: local companies should take on only those tasks they can do now but build up capacity to do more later.

Push manufacturing

South Africa, with its developed infrastructure and links to global markets, should be poised to move from the shipment of unprocessed minerals to a more diversified, manufacturing-led economy. And the government could offer critical help here, according to Iraj Abedian, chairman of Pan-African Capital Holdings: “The rand exchange rate has made South Africa a manufacturing economy that is cheaper than China […]. South African policy-makers need to make the environment more stable so that manufacturing can get off the ground.”

Mbuyiseni Ndlozi, an EFF member of parliament, also calls for diversification. He says he wants to see a strong state role: “There is a mining crisis. We have to move beyond commodities […]. The most labour-intensive sector you should invest in as government is agriculture.”

Anglo American’s Cutifani says the forces for change in the resource businesses go far beyond commodity prices: there is the rise of disruptive technology, the gear change in China’s economy that will influence both the type and volume of raw materials needed, and climate change that will affect the viability of some natural resource operations.

New approaches, according to Cutifani, could include measures to make communities involved in mining more sustainable. The growing use of digital technology and data will make mining smarter and more cost-effective but it will employ far fewer people.

Another wake-up call came from Michael Power, a scenario guru for Investec Asset Management: “Unlike a few years ago, many are now feeling depressed about Africa’s economic prospects, with the current problems reflect- ing changes in conditions exacerbated by local structural and cyclical issues,” he told corporate chiefs at a private break- fast during the Mining Indaba.

Investors have to realise “that the Africa story is not just about buying into local consumer stories that reflect good demographics, urbanisation and the spread of consumer finance, aided by the mobile phone,” he said. He predicted there would be five game-changers this year: China, commodities, currencies, creditworthiness and climate change.

India next

The next upturn in the global economy and mining is likely to be driven by India, said Power, but that could take another seven years or so. That prognosis is of great interest to East Africa, which focuses on the hyper economies of China and India across the Indian Ocean.

Power argues that East Africa’s economies – partly because of their advanced regional integration led by Kenya, Uganda and Rwanda – are a good fit with Asia. Their economies are more diversified, less oil- and mineral-dependent than most others, with serious manufacturing in Ethiopia and Kenya, and they are at the centre of the global mobile-money revolution that started in Africa.

Regional integration and technological innovation are also critical for Rwanda, restricted both by its small domestic market and limits on the growth of its agricultural sector. The region – with Ethiopia’s Grand Renaissance Dam, Kenya’s geothermal power, Tanzania’s offshore gas and plenty of solar and wind power potential – is also fast moving towards energy independence.

All this is pushing policy-makers in resource-dependent economies in other regions to look more closely at trends in East Africa, as regional economies are drawn together to make more viable markets in an effort to cut their chronic dependence on revenues from commodity exports.

{kind=link}