Outlook stable

Ghana

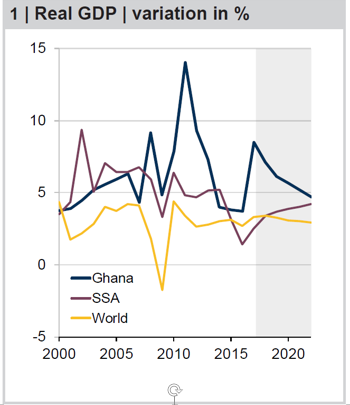

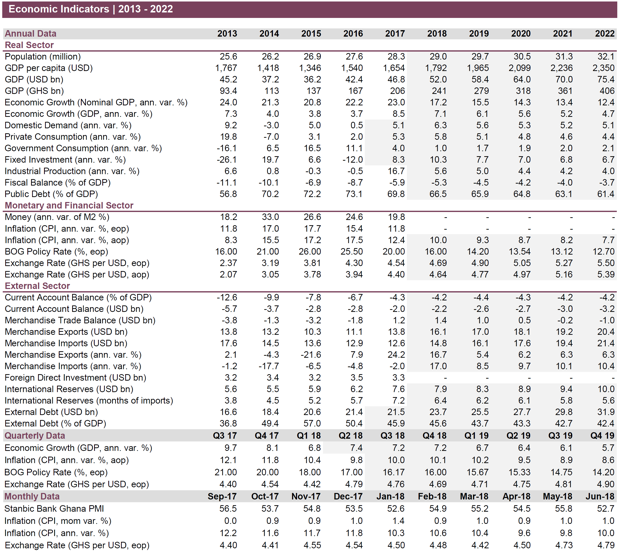

First-quarter annual growth came in at 6.8%, as the economy continued to gradually lose momentum at the outset of the year, after growth hit a five-year high in 2017. A subdued performance by the non-oil sector was mostly behind the slowdown; considerably weaker growth in the industrial sector weighed on economic activity, driven by a feeble increase in manufacturing production that mostly offset strong growth in mining and quarrying activity. In addition, agricultural output growth fell sharply in Q1, partly driven by a weak harvest. Meanwhile, second-quarter prospects point to a further slowdown in growth; the PMI fell to a five-month low in June, whereas inflation jumped back to double-digit territory in the same month. Together with a weaker cedi, higher inflation signaled potential headwinds for sustained domestic demand growth.

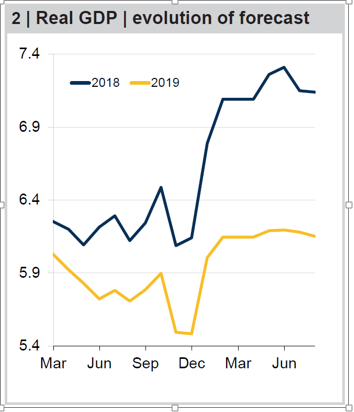

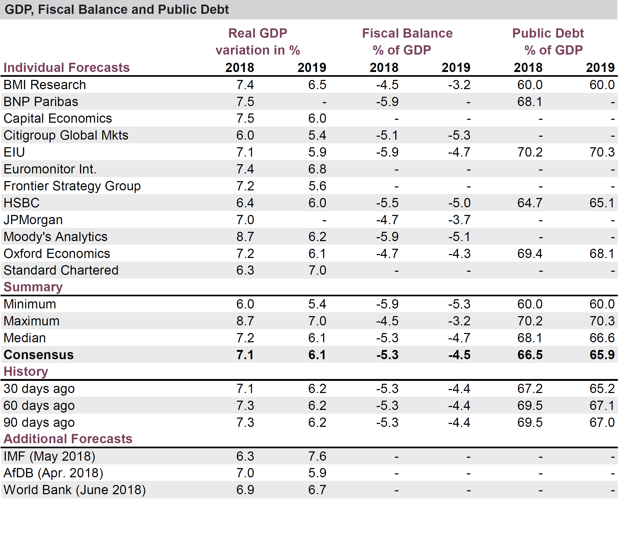

Despite a soft first quarter, exports should drive the economy forward this year amid a favorable outlook for gold, cocoa and oil prices, and an expected increase in domestic oil output. Meanwhile, healthy private consumption and robust investment activity growth should keep domestic demand strong in 2018. FocusEconomics panelists see GDP expanding 7.1% in 2018, which is unchanged from last month’s forecast, and 6.1% in 2019.

Inflation rose for a second consecutive month in June, coming in at 10.0% (May: 9.8%) on stronger non-food inflation. As a result, inflation now rests at the upper bound of the Central Bank’s inflation target of 8.0% plus or minus 2.0 percentage points. FocusEconomics panelists see inflationary pressures carrying on in the short-term. They project inflation will average 10.0% in 2018, which is down 0.1 percentage points from last month’s forecast, and 9.3% in 2019.

The Bank of Ghana decided to slash the key policy rate by 100 basis points to a record-low 17.00% on 21 May, citing the stabilization of inflation and exchange rate expectations as the basis for the cut. The probability of another rate cut at the upcoming meeting on 18 July seems somewhat low, as inflation picked up pace in both May and June. FocusEconomics panelists expect the monetary policy rate to end 2018 at 16.00% and 2019 at 14.20%.

On 13 July, the cedi traded at 4.78 per USD, a weakening of 2.1% month-on-month, as the U.S. dollar remained elevated following the Federal Reserve’s rate hike in mid-June. Nevertheless, both the Central Bank and our panelists expect stable inflation and rising oil production to help the cedi recover some lost ground this year. FocusEconomics panelists project the cedi will end 2018 at 4.69 per USD and 2019 at 4.90 per USD.

REAL SECTOR | GDP growth moderates in Q1

A provisional estimate released by Ghana’s Statistical Service on 27 June shows that the economy kicked off 2018 on softer footing. GDP expanded 6.8% annually in Q1, after clocking impressive growth rates in the second half of 2017 (Q3 2017: +9.7% year-on-year; Q4 2017: +8.1% yoy).

The slowdown was driven by a sizeable drop in industrial production growth, which slowed from 17.5% year-on-year in Q4 to 9.6%. Industrial production decelerated despite the sustained momentum in mining and quarrying output growth (Q1: +28.0% yoy; Q4 2017: +43.9% yoy) which came on the back of Ghana’s buoyant oil sector. In addition, agricultural output growth also decelerated markedly at the beginning of the year, coming in at 2.8% in annual terms in Q1 (Q4 2017: +8.5% yoy) due to weaker crops. Q1’s print marked the weakest readings for both the industry and agricultural sectors since Q4 2016.

The performance of the services sector, which accounted for just over 60% of GDP in Q1, was comparatively healthier, with the expansion in the first quarter (Q1: +5.2% yoy) markedly above Q4 2017’s 3.4% growth. Double-digit growth in the information and communication sub-sector led the expansion, offsetting a notable contraction in the finance and insurance sub-sector.

In quarter-on-quarter seasonally-adjusted terms, the economy expanded 1.5% in the first quarter, decelerating from the previous quarter’s 2.1% increase.

Looking ahead, the recovery should be sustained but moderate somewhat as the base effect from an increase in oil and gas production last continues to evaporate. Nevertheless, the continued expansion of the non-oil sectors and robust domestic demand amid easing inflationary pressures are projected to keep activity buoyant over the coming years.

FocusEconomics panelists expect GDP to expand 7.1% in 2018, which is unchanged from last month’s forecast, and 6.1% in 2019

REAL SECTOR | PMI drops substantially in June but remains in positive territory

The Stanbic IBTC Bank Ghana Purchasing Managers’ Index (PMI) dropped to 52.7 points in June from 55.8 points in May, marking the lowest reading in five months. Nevertheless, the index remained above the 50-point threshold that separates improvement from deterioration in private sector business conditions.

The weakening in the PMI was driven by slower output growth, which fell from a survey-high in May to a five-month low in June. Output eased in the face of moderating new orders growth, which fell to a year-to-date low in June, amid signs of inflation picking up pace again after several months of moderation. Higher oil prices and the cedi’s depreciation against the U.S. dollar in recent months buoyed inflationary pressures in June, which led to higher input costs that were passed on to consumers. Following the trend, purchasing activity decelerated in June against the backdrop of rising inflationary pressures and input costs. Meanwhile, businesses continued to expand new hiring in June, allowing them to clear some backlogs of work; outstanding business declined by the greatest extent since October 2017.

Commenting on the report, Phumelele Mbiyo, Head of Africa Research at Stanbic Bank, noted:

“The PMI is broadly consistent with macroeconomic data that shows the economy growing strongly. The hint of pricing pressures indicated by the survey results might be confirmed by a deceleration in the pace of decline in actual consumer price inflation.”

FocusEconomics Consensus Forecast panelists expect fixed investment to expand 10.3% in 2018, which is up 1.8 percentage points from last month’s estimate, and 7.7% in 2019.

MONETARY SECTOR | Inflation edges up in June

Inflation creeped up again in June, coming in at 10.0% (May: 9.8%) and marking the second month of acceleration after reaching an over five-year low of 9.6% in April. The result was driven by higher prices for clothing and footwear, recreation and culture, and transport, which offset more moderate price increases for food and non-alcoholic beverages. As a result, inflation moved to the upper bound of the Central Bank’s inflation target of 8.0% plus or minus 2.0 percentage points. Meanwhile, annual average inflation inched down to 11.0% in June, from 11.2% in May, marking the lowest print in over four years.

On a month-on-month basis, consumer prices rose 1.0% in June, unchanged from the previous month’s reading.

FocusEconomics Consensus Forecast panelists expect inflation to average 10.0% in 2018, which is down 0.1 percentage points from last month’s forecast, and 9.3% in 2019.

{kind=link}