The use of technology to transact in the utility service space is elevating the electricity market by influencing demand for power through the ease of transacting.

In Uganda, as in many countries in sub-Saharan Africa, electricity utilities experience revenue collection challenges due to consumers delaying or not paying for the electricity they have consumed. This results in cash flow challenges and/or financial losses to power utilities. However, the advent of technology and specifically mobile applications is now at hand to address one of the major challenges faced by the distribution utilities – revenue collection.

Before the mobile payment innovation, payment for electricity was mainly effected through commercial banks and utility service centers. As the mobile money revolution gained traction, the industry harnessed this technology to facilitate payment by consumers for electricity.

The nine electricity distribution companies in Uganda, the two largest, Umeme Limited and Uganda Electricity Distribution Company (together with a market share of over 97%), adopted mobile money services to receive payments from electricity consumers. With the benefits of using mobile money, it’s expected that all distribution companies in the east African country will adopt the technology in the short term. This introduction and adoption of mobile money payment platforms facilitated realization of the following benefits:

To consumers

Electricity consumers have benefited from the convenience of making payment for bills on their mobile phone in the comfort of their homes, and from accessibility to the outlet network of mobile money throughout the country.

Mobile payments have saved consumers both time and money. In rural areas, where household settlements are sparsely populated, consumers (before implementation of the mobile payments) would travel long distances to distribution utility service centers to effect payments.

For utilities

Improved revenue collection since the distribution utilities have been able to reduce the time taken to collect revenue (because of the convenience of mobile payment systems) has reduced working capital requirements. In addition mobile payments, among other factors, have increased and improved revenue collection rates by distribution utilities, which were recorded as 91.0% in 2012 to 99% in 2017. There is also a reduction in operation and maintenance costs associated with the establishment of service centers to manage the clientele.

Economic contributions of mobile payments to the electricity industry

Customer growth using mobile payments

Arising from benefits and according to ERA, the number of electricity consumers paying for bills using mobile money increased from about 15,000 consumers in 2012 (representing 2.9% of the total consumers) to about 755,317 consumers in 2017 (representing 52.2% of the total consumers).

Revenue collections and growth

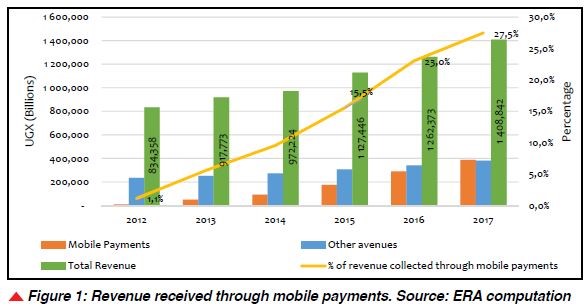

By 2017, about 27% of the revenue collections of the distribution companies was received through mobile payments, a significant increment from 1% in 2012 (Figure 1). This demonstrates the convenience as opposed to bank payments or walk-in at service centers.

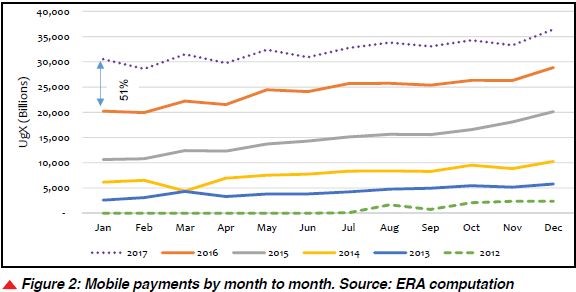

Mobile payment collections by month (Figure 2) show increments in collections by months across years, with the peak payments observed in December, 2017.

Mobile payment is not without challenges

Despite the benefits, mobile payments do face and pose challenges:

System downtime: service and agent system downtime does occur. When the system is down electricity consumers cannot buy units, leading to loss of revenue for the utility.

Fraud: mobile money transactions are open to fraud. Agents are transacting large sums of monies and don’t always have proper security (such as firewalls) in place, making them vulnerable to cyber-attack.

Wrong account numbers: when effecting payments for electricity, it is common for electricity consumers to input/key in incorrect account/meter numbers, leading to loss of funds. Reversing a transaction to an incorrect account/meter is burdensome.

Transaction threshold for industrial consumers: there are transaction amount limits of $3,000 per day. Existence of this threshold constrains industrial electricity consumers from using mobile money to purchase the large number of units they require to conduct their day-today activities.

Privacy and data security: mobile money, like other financial services, has privacy and data protection issues. In Uganda the privacy and data security concerns are partly addressed through the Financial Institutions Act and the Uganda Communications Act. These regulations do not fully address the data security concerns relating to mobile money. This data includes transactions, payer, payee, items purchased, transaction values, and account balances.

Mobile money regulatory framework: one of the major challenges facing the mobile money services is the regulatory environment and absence of a well-defined regulatory regime. Existence of an effective regulatory framework fosters competition, encourages innovation, attracts investments, and ensures convenient and secure services through the establishment of a level playing field, as has been witnessed in the electricity supply industry.

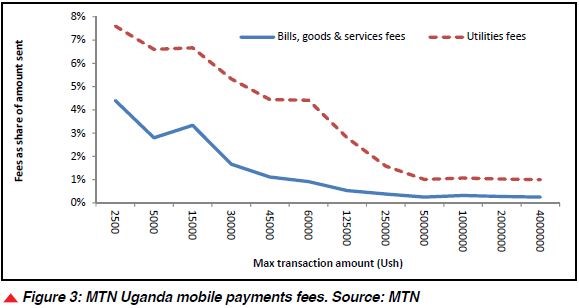

Service fees: the other challenge is that mobile payment fees for utilities are higher compared to payment of goods and other services (Figure 3). In conclusion, embracing and harnessing technology is the solution to the economic development challenges in sub-Saharan Africa. Electricity utilities and regulators in the region must embrace technologies in all areas: not only for revenue collection but also for energy loss reduction, prepayment metering, installation of off-grid and mini-grid projects to address low access to electricity, and the management of supply and demand through automatic meter reading. ESI

Mr. Vianney Mutyaba