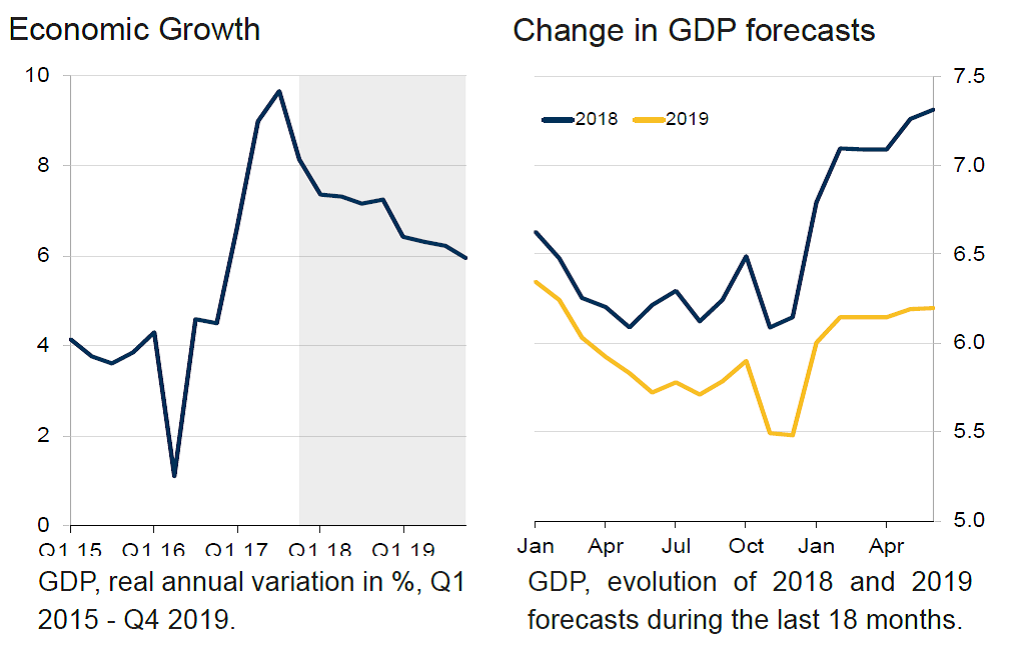

The economy appears to have remained buoyant at the beginning of the year, keeping up the momentum that brought full-year GDP growth to a five-year high in 2017. Firm PMI readings in the January–April period point to a sustained expansion in business conditions, likely on the back of robust domestic demand, which was buttressed by retreating inflationary pressures and easing monetary policy in the period. However, the contribution of the external sector slowed at the beginning of 2018 despite elevated commodity prices, with export growth falling to single digits in February. The cooling could be signaling a potential slowdown in the country’s industrial production sector, due to a weakening mining outlook.

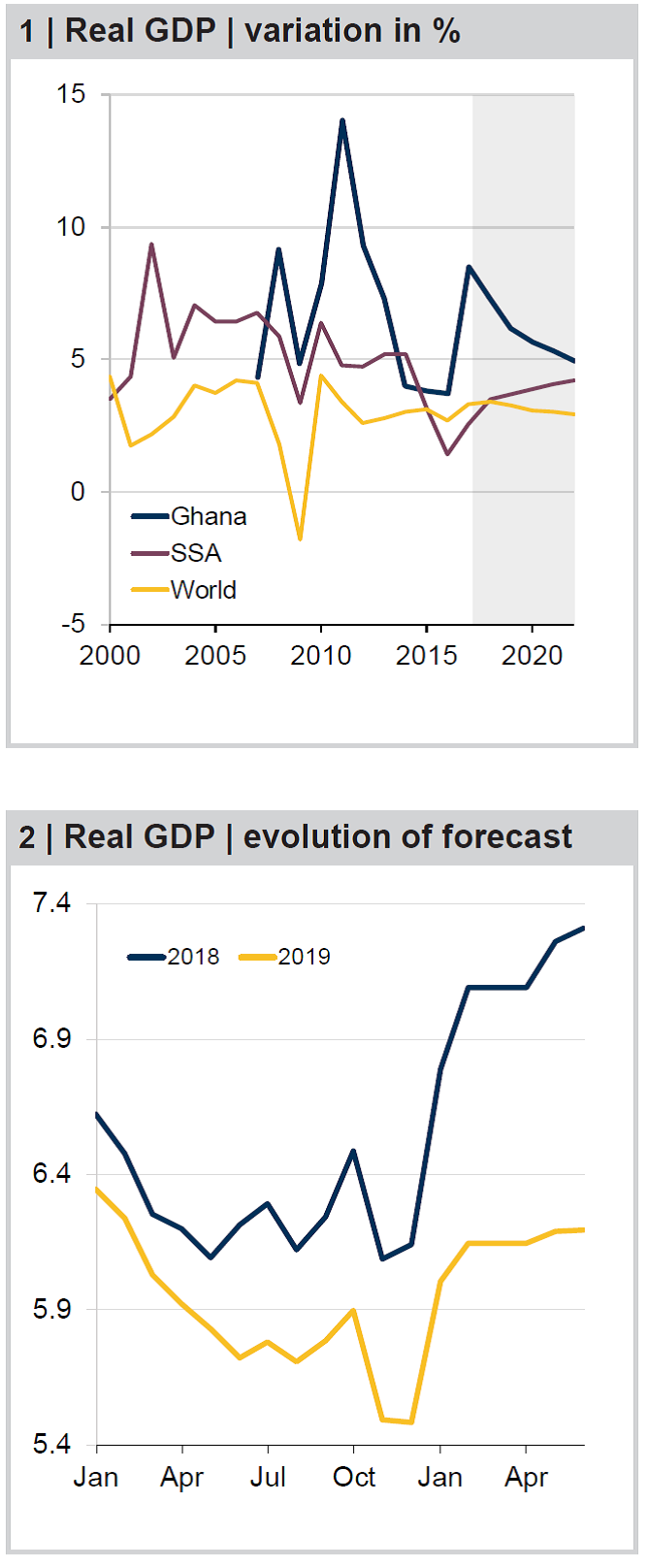

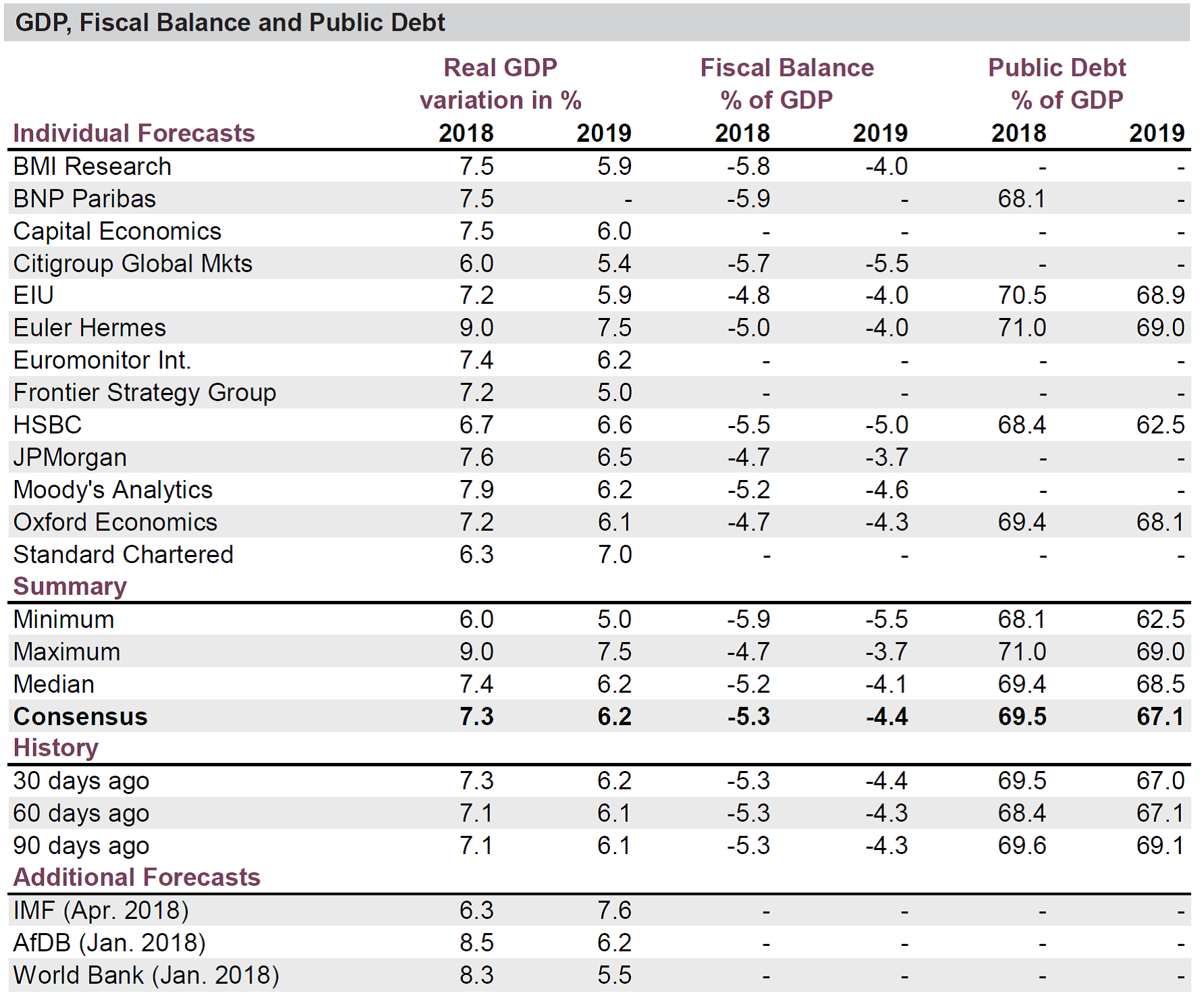

Robust household consumption and healthy investment activity should buoy domestic demand this year, fueling overall economic activity. Commodity exports, including of oil, gold and cocoa will, however, continue to be the backbone of the economy, and an expected favorable global commodity price outlook and a projected increase in oil production should drive growth this year. FocusEconomics panelists expect GDP to expand 7.3% in 2018, which is unchanged from last month’s forecast, and 6.2% in 2019.

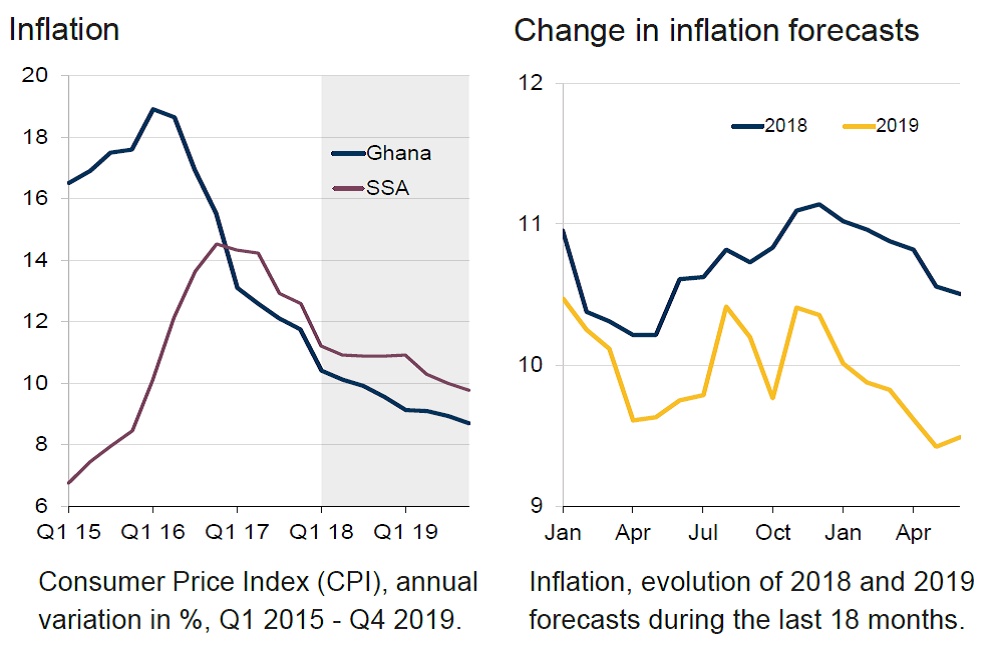

Inflation moderated to a nearly five-year low of 9.5% in April, down from the previous month’s 10.4%. As a result, inflation moved to within the Central Bank’s medium-term inflation target of 8.0% plus or minus 2.0 percentage points. FocusEconomics panelists expect a further easing of inflationary pressures going forward, and they project inflation averaging 10.0% in 2018, down 0.1 percentage points from last month’s forecast, and 9.0% in 2019.

The Bank of Ghana decided to slash the key policy rate by 100 basis points to a new record low of 17.00% at its monetary policy meeting that concluded on 21 May. The Bank cited stabilization and consolidation of inflation and exchange rates expectations as a basis for the cut. Meanwhile, the probability of another rate cut in the coming months remains high, amid easing inflationary pressures. FocusEconomics Consensus Forecast panelists expect the monetary policy rate to end 2018 at 16.00% and 2019 at 14.20%.

The cedi depreciated notably in recent weeks: On 18 May, the currency traded at 4.63 per USD, weakening 3.99% month-on-month, as the U.S. dollar continued gaining strength on the back of higher U.S. Treasury yields. Nevertheless, both the Central Bank and our panelists expect easing inflation and rising oil production to keep the currency from depreciating more this year. FocusEconomics panelists project the cedi to end 2018 at 4.52 per USD and 2019 at 4.71 per USD.

REAL SECTOR | PMI eases in April

The Stanbic IBTC Bank Ghana Purchasing Managers’ Index (PMI) moderated in April to 54.5 points, down from March’s six-month high of 55.2 points. Despite easing, the reading pointed to yet another improvement in operating conditions, as it remained comfortably above the 50-point threshold that separates improvement from deterioration in private sector business conditions.

Solid new orders growth again drove the headline index in April, forming the basis for an overall improvement in business conditions. Given the backdrop of buoyant demand, which was fueled by the introduction of new products and successful marketing campaigns, backlogs of work surged at the highest rate in the survey’s history. In turn, firms continued hiring more staff in April, which marked the 20th consecutive month of net job creation in the private sector. Meanwhile, despite higher input costs, output prices remained stable in April, ending a nine-month run of rising prices as inflation came in at a record low.

Commenting on the report, Ayomide Mejabi, Economist at Stanbic Bank, noted:

“While many businesses received a strong level of new orders, the rate of growth slowed slightly in April as business activity normalized to more sustainable levels. Interestingly, the output price index showed that the disinflation process already underway in Ghana should continue as food inflation and exchange rate volatility remains benign.”

FocusEconomics Consensus Forecast panelists expect fixed investment to expand 8.5% in 2018, which is up 0.8 percentage points from last month’s estimate, and 8.0% in 2019.

Our panelists see GDP expanding 7.3% in 2018, which is unchanged from last month’s estimate. Panelists project growth moderating to 6.2% in 2019.

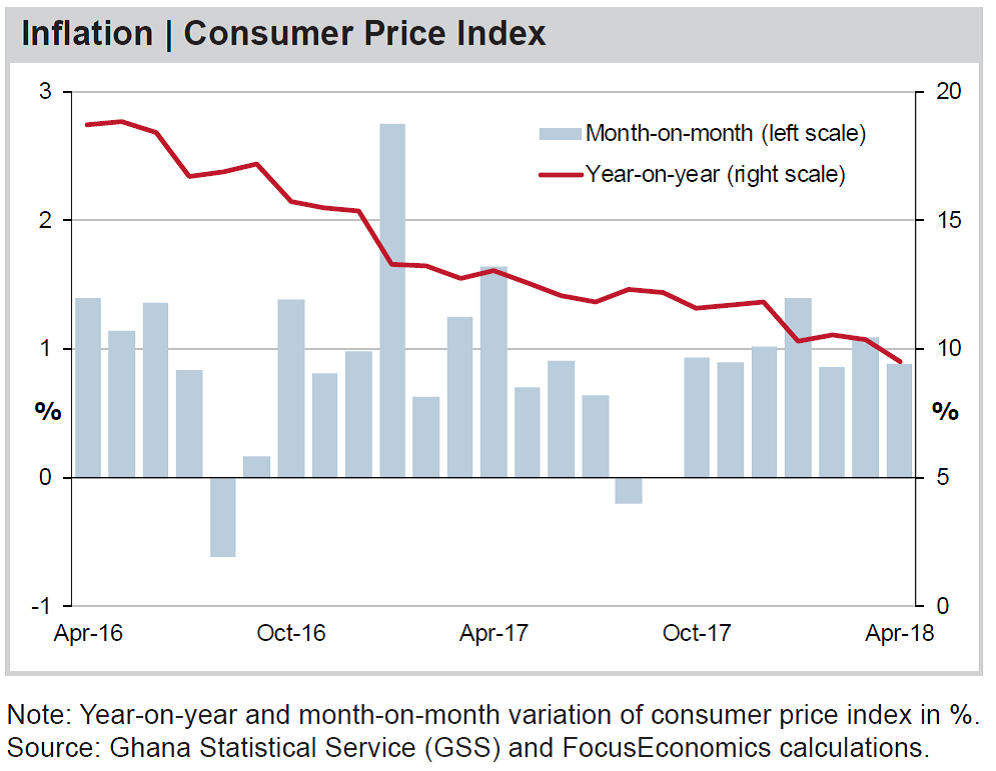

MONETARY SECTOR | Inflation falls to within Central Bank’s target range in April

Consumer prices rose 0.9% over the previous month in April, easing from March’s 1.1% month-on-month increase. The moderation was driven by a notable fall in the price for housing, water, electricity, gas and others fuels from the previous month in March.

Inflation ticked down in April to 9.6% from 10.4% in March. The reading largely reflected a moderation in transport and housing and utilities prices, which was partially offset by an uptick in food prices.

As a result, Inflation moved to within the Central Bank’s medium-term inflation target of 8.0% plus or minus 2.0%. Meanwhile, annual average inflation ticked down from 11.7% in March to a nearly four-year low of 11.4% in April.

FocusEconomics Consensus Forecast panelists expect inflation to average 10.0% in 2018, which is down 0.3 percentage points from last month’s forecast, and 9.0% in 2019.

{kind=link}